Category ►►► Econ. 101

September 25, 2013

Obamunism = Drowning In Debt

Peter J. Tanous presents a grim and grisly future of staggering debt due to the Federal Reserve's "quantitative easing" (QE) -- which itself appears to stem from a bad misreading of John Maynard Keynes. (Is there a good reading of Keynes?)

(I'm certainly no expert on Keynesianism; I never even made it to the 50-page mark in any of its creator's books. But I've read Keynesian analyses -- written by true-believer Keynesians -- that say JMK himself only advocated flooding the market with money when the country being flooded had a very, very small debt-to-GDP ratio... and definitely not when it was already deeply underwater. If any Keynesian expert wants to correct me, please feel free to do so in the comments!)

Under QE, as the Wikipedia article indicates,

The central bank may enact quantitative easing by purchasing a predetermined quantity of bonds or other assets from financial institutions without reference to the interest rate. The goal of this policy is to increase the money supply rather than to decrease the interest rate, which cannot be decreased further.

The last sentence of this paragraph offers a dire warning:

This is often considered a last resort to stimulate the economy.

I wonder whether this mindset, that the government must "stimulate" the economy, is actually the root cause of the fiscal and economic problem in the first place. Perhaps we should consider being more hands-off, helping the "deserving poor" hit by unmanageable financial collapse, and letting Capitalism right the ship in its own time. But be that as it may, that's not the system we have nor likely to have in the near future. So let's return to what is actually happening and the dire consequences quantitiative easing may produce.

The article identifies several risks of QE that can severely damage the American economy:

- The intended result of QE is to flood the economy with cheap money; but another word for "cheap money" is "inflation."

- Because interest rates have dropped precipitously, interest on pensions and savings may not stay ahead of said inflation, leading to a continuing loss of retirement income for ordinary people.

- "The new money could be used by the banks to invest in emerging markets, commodity-based economies, commodities themselves, and non-local opportunities rather than to lend to local businesses that are having difficulty getting loans." We see this today, with stock prices soaring even as wages are stagnant or dropping, employers are cutting hours to push more of their employees into "part time" status, and startups that could have filled the job gaps are depressed because of the lack of lending to new businesses.

The recipients of the extra cash under QE tend to be banks, companies that already have ready access to large lines of credit, and homeowners who already have mortgages; consider how many of us have taken advantage of the low interest rates to reduce payments on our existing home mortgages. The article notes, "Economist Anthony Randazzo of the Reason Foundation wrote that QE 'is fundamentally a regressive redistribution program that has been boosting wealth for those already engaged in the financial sector or those who already own homes, but passing little along to the rest of the economy. It is a primary driver of income inequality'."

Massive income inequality typically leads to social dislocation, a two-tiered economy, the loss of belief in opportunity for upward mobility, and ultimately, to more reliance on government handouts -- thus leading to a more big-government paternalism and a citizenry leaning more towards socialism and welfare.

But Tanous notes an even nastier consequenece of QE... one which, rather than being unintentional, might actually be the "hidden agenda" of the Fed's policy of flooding the economy with cheap dollars. From the CNBC piece:

Let me start with a question: How would you feel if you knew that almost all of the money you pay in personal income tax went to pay just one bill, the interest on the debt? Chances are, you and millions of Americans would find that completely unacceptable and indeed they should.

But that is where we may be heading.

That eventuality may be shocking, but it would not be difficult to achieve. QE has driven down interest rates on federal debt to 2.4%; as we have about $12 trillion of such debt, we're paying about $288 billion every year just to service that debt... that is, to pay the interest; we are not, of course, reducing that debt. In fact, it's still increasing and is expected to rise by 2020 to the princely sum of $16.6 trillion.

But the chief danger of QE is that it cannot continue indefinitely, because, as Friend Lee has said, government can set the price but not the cost of goods and services. An excess of money (which is what is meant by quantitative easing, e.g. cheap money, e.g. electronic counterfeiting) cannot be forever suspended overhead. Sooner or later, it must come crashing down.

And when it does, among other dread problems, interest rates will rise again. Obamunists hope that the crash will hold off until a Republican sits in la Casa Blanca, so they can blame the resulting financial carnage (from their own stupid policies) on that luckless bag-holder... just as Democrats tried to blame the 9/11 attacks on George W. Bush.

So how high might interest rates rise? Tanous says that the average interest rate for U.S. debt over the last two decades is actually 5.7%. If interest rates were only to return to the average, then instead of $288 billion per year in interest, we would be paying $684 billion.

But in the meantime, more debt will accumulate up to that $16.6 trillion level by 2020. Thus not only the interest but the principal would rise... and we would actually be paying $946 billion in debt service alone. (Tanous says $930 billion; I'm not sure why the discrepency, perhaps a rounding error.)

In 2012, the entire amount of personal income tax collected by the IRS was $1.1 trillion. Assuming QE doesn't lead to a great economic leap forward -- not even the Feds predict that! -- Americans would soon realize that 85% of their income taxes (or 86%, if you use the $946 billion number) went to nothing but paying interest on the bloated national debt.

Tanous drolly suggests that --

[I]f Americans find out that the lion's share of their income tax payments are going to service the debt, prepare for a new American revolution.

I think that's an understatement. But the scariest uncertainty is whether that revolution will target the real culprits -- the Obamunists, going all the way back to the Progressivist cadres who captured the 2006 election, the ones who broke the economy in the first place... or whether voters will simply (and simplistically) blame whoever is president at the moment -- likely a fiscally conservative Republican trying his best to clean up the awful mess the Left left behind.

If I wasn't utterly convinced of the essential incompetence of the administration and its lickspittels in Congress, of their inability to think beyond a two-year window, I might believe this was a deliberate conspiracy to destroy the American economy, ushering in a new New Deal era of socialism, tyranny, and totalitarianism. The only thing missing would be another "world war" to warp patriotism into slavish devotion to a cult of personality, an American Hugo Chavez.

Fortunately, there is nobody on the Progressivist horizon with enough charisma to fill that role; at worst, we might end up with a Teddy Roosevelt-like, big-government Republican... a Chris Christie, for example. And as bad as Christie might be, he would still be more interested in preserving the Union than "transforming" it.

Hatched by Dafydd on this day, September 25, 2013, at the time of 3:20 PM | Comments (1)

January 10, 2013

The Imperator Misses a Bet

President-for-Life Barack Obama and his Treasury flunkies have concocted a wonderous lotos-dream of an idea. They can't simply print money willy-nilly to reduce the deficit; that's the Federal Reserve's job!

But a bizarre loophole allows them to print -- I mean mint -- a trillion-dollar coin... but only if made out of platinum; evidently, no other chemical element will do.

Their idea is to mint such a coin and stick it in the United States Treasury's account at the Fed. I'm not sure who gets to keep it in his pocket. This would, of course, pretty much eliminate the deficit; after all, the government would just have deposited a trillion dollars in its account -- abra-cadabra, our deficit problems are solved.

But the president and his advisors appear to have missed a huge opportunity... why not simply mint sixteen of those trillion-dollar coins and deposit them all? Voilà, the entire federal debt has just been paid off!

With those sixteen platinum blondes as hostages (is Lady Liberty the new Jean Harlow?), the Fed will cheerfully pump $16 trillion into the economy, in cash-like electronic blips. I'm sure Paul Krugman and other genius economists will assure us that air-dropping sixteen thousand thousand thousand thousand buckaroonies won't affect inflation much; maybe just 100% to 500% per year -- we can live with that. And the One can then take credit for being the first POTUS ever to completely eliminate the national debt. Another spectacular triumph! (All right, except for that old krummhorn Andy Jackson in 1835-1836; but he was an old, white southern racist, so he can safely be ignored.)

Solving great dilemmas is so much simpler when you get to redefine and reprogram all the normal rules of economics, politics, science, and mathematics to suit your own convenience and conceits. Just ask Captain Kirk about that pesky Kobayashi Maru test.

Hatched by Dafydd on this day, January 10, 2013, at the time of 2:30 AM | Comments (3)

January 9, 2013

Best "In a Nuthouse" Explanation of the Year!

Of course, the year is still young...

This is ripped straight from Rich Galen's most recent Mullings; and if you're not reading Mullings -- for free! (but please send a $30 donation at fundraising time) -- you're missing a treat and a wonder.

Here's the bit, sent in by one of Rich's readers; and boy does this just put the federal debt cliff on that old nutshell:

- U.S. Tax revenue: $ 2,170,000,000,000

- Fed budget: $ 3,820,000,000,000

- New debt: $ 1,650,000,000,000

- National debt: $14,271,000,000,000

- Recent budget cuts: $ 38,500,000,000

Let's now remove 8 zeros and pretend it's a household budget:

- Annual family income: $ 21,700

- Money the family spent: $ 38,200

- New debt on the credit card: $ 16,500

- Outstanding credit card balances: $ 142,710

- Total budget cuts so far: $ 38.50

One quibble: I believe the national debt is closer to $16 trillion than $14 trillion -- leaving the "household budget" in dutch for $160,000 samolians, not $142,710; but who's counting? (Certainly not Obama, Geithner, or "Pinky" Reid!) But that just gilds the cake.

I wonder if a simple YouTube of someone pointing at a chart very like unto this one could go viral, and maybe shake the faith of a few Obamolytes?

Hatched by Dafydd on this day, January 9, 2013, at the time of 12:17 AM | Comments (1)

July 2, 2012

Don't They Ever Run Out Of Ink?

Fresh off the press at MSNBC comes a useful article for a change. Manufacturing contracted for the first time in three years, a sign that the companies that make the stuff we buy are anticipating tougher times ahead -- not quite the "private sector is doing fine" assurances that Barack Obama shared with us the other week.

More troubling, however, is how the markets reacted to the news. It's not that I'm wishing for a steep drop, because God knows my 401(k) has been on a roller coaster ride lately; but the assertion that the Fed is cushioning the blow with even more more easy money policies makes me very, very nervous.

The reason? Interest rates are already near zero--which means the only way the Fed can make things "easier" is to -- drum roll, please -- that's right, print more money!

Basically, the administration is continuing to feed the stock market a sugar high in the hopes of keeping the Dow elevated. While this makes things look better in the short term, the time is going to come when all that loose money is going to cause massive inflation. Some predictions have it happening as soon as next year.

Throw in ObamaCare, the expiration of the Bush tax cuts extension in January, and the reams of regulations imposed by Washington since Obama took office, and the picture doesn't look at all good. Hang on to your assets, folks.

Hatched by Korso on this day, July 2, 2012, at the time of 6:42 PM | Comments (2)

December 7, 2011

Lefties Love the Static Quo!

California Gov. Edmund Gerald "Jerry" Brown, jr. (son of former California Gov. Edmund Gerald "Pat" Brown, sr.) is pushing hard for a big, punitive state income-tax hike on "the rich," meaning the top 1% -- who pay nearly 50% of California income tax.

New York Gov. Andrew Cuomo (son of former New York Gov. Mario Cuomo) just cut a deal to raise taxes an extra two percent (from 6.85% to 8.82%) on those earning $2 million per year or more.

And numerous other blue states are seeking to do the same... as is, of course, President Barack H. "Lucky Lefty" Obama (son of no one).

One thing all these economically challenged chief executives have in common is their inability -- or unwillingness -- to grok the idea of dynamic economic analysis, and their subsequent slavish devotion to static analysis. That is, they assume that a new tax policy will not itself alter people's tax-avoidance behavior. Or else they pretend to assume it, as it helps their duplicitous schemes; I lean towards the latter explanation.

Their real or feigned "reasoning" goes thus:

- We have a state income tax of 7% that brings in $10 billion.

- We have a budget shortfall of $2 billion.

- Therefore, all we need do is raise taxes to 8.4%; if 7% brings in $10 billion, then jacking it up by 20% of that 7% -- by 1.4% extra -- will surely bring in $12 billion.

- Problem solved! Q.E.D.

Leave aside for a moment the first obvious point: No such plan has ever or will ever allocate all the extra money to deficit reduction; even if it seems to do so and is actually written into the law, money is fungible... and the state legislature (or Congress) will simply increase other spending... thereby increasing the deficit by even more than it was reduced by revenue from the new tax. But we're not here to talk politics; let's just stick with the tax itself for a moment.

The syllogism above is a perfect gem of static analysis: The politicos argue (honestly or mendaciously) that if 7% raises $10 billion, then 8.4% will raise $12 billion. If we continue the argument, then a state income tax of 14% will raise $20 billion, 50% will raise $71 billion -- and if the state would only have the guts to raise its income tax to 100%, that would firehose a whopping $143 billion into the state coffers!!1!

Which points out (a) the absurdity of the naïve static hypothesis, and (b) the proper use of reductio ad absurdum.

It's clear to anyone with more than a couple neurons to rub together that any increase in tax rates will trigger people to engage in more tax-avoidance tactics. It's a no-brainer. And what socioeconomic group do you reckon is best equipped to legally avoid taxes? Yep, that's what I reckon, too: the rich.

For state income taxes, the absolute best tax-avoidance tactic is (drum roll) to move out of the high-tax state into a low- or no-tax state... of which there are plenty; they're called "red states." Until and unless Democrats begin requiring internal passports for travel -- any month now, I expect -- they can't stop the Evile Rich from fleeing California to repatriate in Nevada or Texas.

But beyond moving, the very, very successful also have the unique ability to restructure their revenue stream, shifting it, say, from ordinary income to capital gains, or from American sources to foreign sources, or to delay receipts until a more favorable tax situation presents itself. If need be, they can forgo salaries and such for years without feeling any pain, living off savings or just mooching off friends (who will expect reciprocity in their own time).

The ne plus ultras can engage in tax-reduction activities, taking advantage of "loopholes" that are, in reality, congressional subsidies to lure rich investors into otherwise unexciting ventures. The rich can get their friends to receive their income for a while, then pay it back later. And of course, the rich can afford legal beagles who are paid a hundred times as much as, and therefore are correspondingly cleverer than, the IRS's own pathetic, also-ran tax lawyers.

The ultra-rich are the very people that municipalities, counties, states, and even the feds are least able to reel back in state, should the designated victims decide they're being overtaxed. The Capitalists always win; in the long run, the invisible hand of the market beats the invisible foot of the government every time.

And if worse comes to worst, the little Monopoly guy can just buy a few more congressmen.

Ergo, since such surcharges on the rich are notoriously uncollectable, static economic analysis is as futile a gesture as passing a law declaring pi to be equal to 3.0 (which the state legislature of Indiana, I believe, nearly did); as futile as passing a law declaring that the United States will return to the carbon footprint it had in 1980. Trying to repeal the laws of economics is like trying to repeal entropy: You can make a good show of it for a geological microsecond; but in the end, you're left with nothing but a big bag of fully expanded hot air.

By contrast, those of us willing to use dynamic analysis -- where we assume that human beings will actually respond intelligently to stimuli -- then we already know what happens when states lower, rather than raise, their taxes, whether personal, business, or capital gains, as well as when states reduce regulations and defund the unions (including public-empoyee unions): Money, talent, genius, and especially people pour into the newly financially attractive state, the new free-trade zone; this in turn causes an economic sonic boom.

But don't expect any of that from elected liberals. I've long been convinced that they're neither stupid nor ignorant of economic laws; they just reject market reality and substitute their own, imposed by executive fiat.

That, in a nuthouse, is what Michael Barone means by calling Obamunism "gangster government."

Hatched by Dafydd on this day, December 7, 2011, at the time of 1:01 AM | Comments (3)

August 30, 2011

The New York Times Defines "Fiscal Conservative"

Just in case you weren't sure of the definition, the New York Times shows us the perfect "fiscal conservative" in Yoshihiko Noda, incoming Prime Minister of Japan:

Yoshihiko Noda, a down-to-earth fiscal conservative, was elected prime minister by the Japanese Parliament on Tuesday in the sixth change of leaders in five years, a period of mounting economic and social challenges to the world’s third-largest economy. [Emphasis added - DaH]

And what fiscal policies does this plucky, self-deprecating, "down-to-earth fiscal conservative" intend to enact to earn that title? The Times clarifies:

In his previous role [as finance minister], he orchestrated multiple interventions in currency markets to weaken a strong yen that has battered Japanese exporters....

As a fiscal conservative, he is one of few within his party to suggest that raising taxes might be necessary to rein in Japan’s deficit....

Mr. Noda “will most likely temper his fiscally hawkish stance, which other candidates were loath to espouse, even as he champions an eventual return to fiscal responsibility,” Naomi Fink, a Tokyo-based strategist at the investment house Jefferies, said in a note....

Mr. Noda has said that he will stick to [outgoing Prime Minister Naoto] Kan’s promise to gradually phase out nuclear power, but that it remains necessary in the short term to prevent electricity shortages that could further cripple the economy. [Emphasis added - DaH]

All right, I think I've got it. A fiscal conservative is a government official who:

- Manipulates currency markets for corporatist political purposes...

- Raises taxes on a shattered citizenry during a terrible recession and ongoing disaster recovery...

- Offers, as the cornerstone of his energy policy, to eliminate (on grounds of eco-hysteria and radical enviromentalism) efficient, highly productive, and clean nuclear power, which is already up and operating, to be replaced (when?) by what, oil and coal, which must be imported at enormous cost, and the infrastructure for which Japan does not even possess? More likely by "green energy": windmills, solar cells, or perhaps banks of perpetual-motion machines to power the island nation...

- And who sees "fiscal responsibility" as a vague and distant goal he might embrace... "eventually."

Yessiree, that's the kind of steely-eyed fiscal conservative the Little Old Grey Lady pines for, in America as well as abroad.

And let's add one more qualification: Japan's Yoshihiko Noda is definitely not one of those slope-browed, slack-jawed, snake-handling, tongues-speaking, science-rejecting, theocratic "Christianists" who lurk in the United States; I'm certain he rejects "either-or" dichotomies: Right and Left, right and wrong, economic and uneconomic, true and false.

If Noda is like his brethren in the Diet, he sees the world in shades of grey, a twilight zone where the wild things are never quite asleep but never fully awake. Noda is certainly from one of the good religions that reject harsh, Judeo-Christian values -- Buddhism, Shinto, Atheism, Communism... something into which a man like Bill Keller can sink his teeth!

Perhaps now we understand Keller's urgency in getting to the bottom of all this "Christianity" stuff rampant among Republican candidates for President: Keller is still searching for those elusive, Times-approved "fiscal conservatives" in the GOP.

Hatched by Dafydd on this day, August 30, 2011, at the time of 2:16 PM | Comments (0)

August 19, 2011

The Permanent Floating Unbalanced Budget Act of 2011

Aaron Worthing, guest blogger at my old stomping grounds of Patterico's Pontifications, draws our attention to the well argued and very persuasive case against a balanced-budget amendment (BBA) by political scientist Carson Holloway of Public Discourse. I was never really on board the federal balanced-budget amendment; it has always struck me as being magical thinking, utopianism -- pass an amendment, and all our spending problems will softly and suddenly vanish away.

(I liken this sort of thinking to Franklin Roosevelt declaring "freedom from want" and "freedom from fear" to be basic civil liberties.)

But the Holloway piece has really crystalized my objections to a BBA. Let me try to explain what's so dreadfully wrong with it.

Holloway's point, on a nutshell, is that there is no way to craft a balanced-budget amndment (BBA) such that it neither cripples our ability to borrow when absolutely necessary, nor allows, under cover of a ficticious "balanced budget," the same unrestricted borrowing for frivolous political reasons that Congress enjoys today. No matter how it's crafted, it will de facto sink into one fallacy or the other (I'm not sure which is worse).

Not only that, but the mere existence of a BBA in the Constitution practically compels Congress to jack up taxes whenever it overspends, probably with wide, bipartisan support: The socialist Left votes to raise taxes because, well, they always want to do that; and big-government Republicans follow suit for reasons of "fiscal responsibility." Can't violate that BBA!

Most likely, "responsible" congressmen will pass enabling legislation that automatically triggers tax hikes if the budget remains unbalanced in a fiscal year; and I can easily imagine a Democratic majority deliberately overspending, precisely in order to trigger that hike, under cover of "constitutional prescription."

Our problem isn't the lack of a BBA; our problem is that individual voters aren't holding their congressman's nose to the fire on limitless federal borrowing and spending, to infinity and beyond.

Or rather, they haven't in the recent past held Congress accountable; we took a huge step towards fiscal sanity last November and are poised to do so again in 2012. My friend and worth co-conspirator Brad Linaweaver recently sent me an e-mail bemoaning the fact that all political parties seem to have to "reinvent the wheel" every generation; and of course, Brad is absolutely right. I believe this is one of those instances, and there's nothing we can do but wait for the renaissance -- which is coming fast and strong, as witness the popular front for Capitalism... i.e., the tea-party movements.

But there is another point to be made beyond Holloway's argument: No real BBA (with teeth) has a chance in Hades of passing the current Congress or any other in the future. The only way a BBA will pass with a two-thirds vote in both House and Senate is if it's so watered down, its only purpose is to give cover to the very fiscal irresponsibility it purports to curtail. For evidence, look how easily states, which generally do have constitutional balanced-budget requirements (like my home state of California), can skirt around them by either manipulating the budget to make it facially appear to be in balance, no matter what the reality; or by simply ignoring the state constitution altogether. Not only is a BBA no panacea, it's not even a good placebo!

Worse, fighting tooth and nail for a BBA is a distraction from the real work of reining in Congress; it drains money, energy, time, and political capital that could be better utilized rolling back Obamunism. Democrats would be overjoyed to see the focus of the 2012 campaign shift from Obama's abominable economic record to a partisan tussle over a BBA... especially with the Left's proven talent at monkeying with statutory language and finding friendly judges to reinterpret out of existence any real restriction on federal power. Instead, we need to spend our considerable resources getting rid of the current squatter at 1600 Pennsylvania Ave., along with his gangster government (as Michael Barone dubbed it), and cleaning out the cesspool of socialism and loony leftism in Congress -- on both sides the aisle, alas.

So let's boil the cabbage down:

- It's impossible to enact a BBA that would really work, at least in the present environment; it's utopian wish fulfillment to think some constitutional amendment will be a "magic bullet" that will solve our economic crisis.

- In the long run, the crusade to implement a BBA would cripple our ability actually to solve our terrible fiscal and economic crisis by sucking up vital political and financial resources better spent on voting the thugs out of office; it substitutes wheel spinning for actual progress, in the proper meaning of that word, away from "liberal fascism" and towards individualism, Americanism, and Capitalism.

- And in the very short run, it would remove the spotlight from liberal corruption, incompetence, and socialistic experimentation and focus it instead upon Republican "radicalism," almost certainly giving the DNC a huge boost at the ballot booth in 2012.

If a BBA becomes the main Republican economic platform plank, then I predict we will only barely retake the Senate, may actually lose seats in the House -- and Barack Obama will be easily reelected, running against "radical Republicans" who want to write wartime insolvency and automatic tax hikes into the Constitution.

It's hard to think of a worse economic strategy, for the election and for the country.

Hatched by Dafydd on this day, August 19, 2011, at the time of 3:44 PM | Comments (1)

July 13, 2011

Look What We Made the Obamacle Do, Part Two

I seem to have dropped a casual bombshell in the sister-post to this, and I ought to cite a source.

After writing the following --

Money comes into the American treasury all the time: quarterly tax payments, corporate taxes, employee withholding, sales of government property, fees, licenses, and so forth. I understand that such continuous income greatly exceeds the bare-bones payment obligations of the United States government -- entitlement payments and debt service. In other words, we have enough revenue to meet those obligations; just not enough to meet them in addition to all the other expensive projects that the Obamunists want to fund at the same time...

-- I received a comment from a frequent commenter who raised the obvious question: Was my back-of-the-thumbnail guesstimate about income and outgo correct? MikeR asked,

You made a claim that there is enough money to cover our bare-bones obligations. I have heard otherwise: That in the month of August, we would essentially have to choose between paying our soldiers, Social Security, and debt service. Did you have a source?

Ask and ye shall receive. I found this on the American Spectator blog, posted today:

But, assuming the debt limit is reached and the Treasury has the power to privilege certain bills over others, there's no doubt that it's within it's power to pay Social Security recipients. The federal government will take in about $172 billion in August, and owe roughly $307 billion. It will have no problem paying the interest on the debt (about $30 billion) and Social Security recipients (about $50 billion).

But what about "paying our soldiers?" The author of the Spectator blogpost, Joseph Lawler, digs deeper:

Bloomberg Businessweek has created a debt ceiling prioritization calculator, using figures from the Bipartisan Policy Center. Using broad categories, it shows which items the government could continue to fund past the deadline while avoiding a default on the debt. By BPC's calculations, it would be possible to continue paying not only for Social Security and the interest on the debt, but also Medicare, Medicaid, unemployment insurance, active duty military pay, TANF [welfare], food stamps, and Homeland Security emergency preparation and response, with billions left over just in case.

Joseph Lawler is the managing editor of the American Spectator; Bloomberg L.P., which publishes Bloomberg Buisinessweek (formerly BusinessWeek), is nearly entirely owned (88%) by Michael Bloomberg, the current Mayor of New York City and a flaming Democrat, for all that he ran for the mayorship as a "Republican." He, his company, and the magazine are hardly likely to tilt towards tea partiers, conservatives, or actual Republicans. I think it safe to trust them all on this point, which constitutes an admission against the Left's interest.

(To be a compleat completist, another commenter, LarryD, posted much of this same information in a comment to the previous post; and MikeR himself found a similar story here.)

Just remember: When in doubt, always trust Big Lizards; we may not always be right, but we're never wrong. (And Power Line. And Patterico's Puntifications, of course; trust them too. And even Beldar, when you can scrape the crust off'n him; but that's a whole 'nuther box of fish.)

Hatched by Dafydd on this day, July 13, 2011, at the time of 4:59 PM | Comments (5)

July 12, 2011

Look What We Made the Obamacle Do!

First it was "Hope and Change," where any kind of change would make things better, any government spending at all would be "stimulative," and hope arose from the mere fact that a man who called himself "post-partisan" and "post-racial" had planted himself in la Casa Blanca. Under his reign, the oceans would subside, the Earth would heal, and like Milo Minderbinder's M&M Enterprises, everybody would have a share.

This idyllic intro-interlude quickly morphed into "gangster government," as Michael Barone put it: a lethal combination of legal bribery from unions and other special-interest groups, followed by wholesale privileges (literally, "private laws") granted to favored constituencies, from auto-worker unions, to teachers, to gays, to federally privileged minorities, to Silicon Valley billionaires, to silicone-mountain Hollywood elites. The president had discovered that democracy is messy, and even those who disagree with Obama are allowed to vote, protest, organize, and voice their opinions.

Faced with such disunity and "chaos" coming from bitter people who cling to their religion and their guns, what was a newly anointed Keeper of the Vision supposed to do? Naturally he had to turn to criminal mobs to appease the liberal mobs who made him -- and who could break him just as easily.

But at last, after years of increasingly dirty (and incompetent) governance coupled with crony "capitalism," the administration of Barack H. Obama slithered into its third and terminal phase: extortion government, in which the President of the United States directly threatens to inflict grievous damage, in a planned and calculating way, upon the most vulnerable of his own people -- unless his political opponents kow-tow to his every demand. (Actually, as Barack Obama considers himself a "fellow citizen of the world," perhaps he doesn't consider them "his people" in the first place.)

In a sense stronger than merely symbolic, Barack Hussein Obama has become Maximilien François Marie Isidore de Robespierre, architect of the French Revolution, the bloodiest community-organizing mob action in history.

Witness: France during the Terror had the guillotine, the "national barber;" America, held hostage, has the deficit -- the national credit card. The administration has maxed out the national credit card (even gone over the limit), and the president is beside himself that he cannot continue charging, charging, and charging to pay for his caviar tastes in government largess.

So today, in a fit of pique, Obama threatens that unless Republicans agree immediately to a Brobdingnagian hike in the national credit card's credit limit and to trilliions of dollars in new taxes and spending, he will deliberately, and with malice aforethought, refuse to send out Social Security and Veterans Benefits checks.

From CBS:

"I cannot guarantee that those checks go out on August 3rd if we haven't resolved this issue. Because there may simply not be the money in the coffers to do it," Mr. Obama said in an interview with CBS Evening News anchor Scott Pelley, according to excerpts released by CBS News.

"Look what you made me do!"

But of course, the administration is responsible for all federal spending. Congress can only appropriate; it's up to the Executive actually to send out the checks. And that means the president has the legal authority and obligation to prioritize spending.

In this case, he has the duty to privilege certain spending -- interest and principal payments to bond holders and "entitlement" payments to seniors and veterans, among others -- over other types of spending, including payments to doctors and hospitals under ObamaCare; block grants to states; foreign aid; funding of Fannie Mae and Freddie Mac, paying vendors and federal contractors; paying for travel by government employees (including the president, Mrs. President, and their posse/entourage); money to the National Science Foundation, the National Institutes of Mental Health, the Corporation for Public Broadcasting, and every other federally funded foundation or institute (no matter how worthy); and even paying federal workers.

Not to mention the hundreds of billions of dollars appropriated by Congress every year for porkbarrel projects in the districts of powerful representatives and senators.

Money comes into the American treasury all the time: quarterly tax payments, corporate taxes, employee withholding, sales of government property, fees, licenses, and so forth. I understand that such continuous income greatly exceeds the bare-bones payment obligations of the United States government -- entitlement payments and debt service. In other words, we have enough revenue to meet those obligations; just not enough to meet them in addition to all the other expensive projects that the Obamunists want to fund at the same time. (What's most galling, of course, is that Barack Obama himself and his cronies in Congress are the very culprits who brought on this terrible financial catastrophe in the first place. "Look what I made you make me do!")

The obvious solution presents itself.

Every large corporation must have a budget; and every such budget must, among other requirements, prioritize the corporation's financial obligations: What gets paid first? What gets paid second, third, nth? I suspect that if a publicly traded corporation was so mismanaged that it didn't even have a contingency plan for what bills to pay if it experienced a sudden revenue shortfall, not only would it be liable for massive lawsuits, but the SEC and the Justice Department might open a criminal investigation of the corporate officers.

Thinking of the federal government as the nation's largest (if not the world's largest) corporation, then mustn't it, too, have a heirarchy of payments to guide the president during a temporary shortfall? Isn't the obvious lack of such an emergency plan, resulting in threats to withhold pledged funds to those who could literally die from such embezzlement -- which is what the president's threat amounts to -- the very definition of financial malfeasance and nonfeasance?

But this sort of hysterical extortion is the liberal's stock in trade. I cannot begin to count how many times a Democratic governor or mayor has responded to reduced revenues by threatening to furlough police and firefighters first, before even considering laying off the thousands of non-essential government workers, from state license form filler-outers and scrutinizers, to inspectors who prowl neighborhoods to make sure nobody has the wrong kind of front lawn or too high a fence, to complicated "diversity" (affirmative action) schemes, to pothole repair, to state highway construction, to light rail, to establishment of new state parks, to city-hall barbers, to spiraling billions to state "education" funding.

It's a vile and shabby trick: Pandering to the liberal mob, Obama attacks the weakest and most vulnerable citizens by directly threatening them with penury and starvation unless Republicans cave. "Nice pension you have there; sure would be a shame if something was to happen to it..." Such intimidation of America's own citizens is so thuggish, so antidemocratic, so unAmerican that it easily rises to the level of high crimes and misdemeanors in the meaning of Article II, Section 4 of the Constitution.

Any ordinary person would burn with shame to threaten the old, the sick, and wounded vets just to enact his pet policies, against the clearly expressed will of the people. I can only conclude that Obama's narcissism is so advanced that he has become a functional sociopath -- the anti-Clinton -- literally incapable of feeling anybody's pain, responsive only to his own sense of aristocratic entitlement and his outrage at being thwarted.

Obama's "audacity" is positively brazen; it doesn't even occur to him to conceal his real motivation. He nakedly commands this issue to go away until after his presumed re-coronation next year:

Mr. Obama has repeatedly said he wants a deal that would allow the U.S. to avoid confronting the issue again until after the 2012 elections and vowed on Monday that he would "not sign a 30-day or a 60-day or a 90-day extension."

He insists that both sides "put politics aside" -- and simply enact the Democratic minority agenda. There's post-partisanship for you, Chicago style. What's next? Will President B.O. take a page from the National Lampoon? "If Republicans don't raise taxes and jack up the debt ceiling, we'll kill this dog!"

November 2012 cannot come soon enough. I only wonder... if Barack Obama continues on the path he has trodden for the past two and a half years, will he become the first incumbent president to lose all fifty-seven states?

Cross-posted on Hot Air's rogues' gallery...

Hatched by Dafydd on this day, July 12, 2011, at the time of 4:36 PM | Comments (6)

June 23, 2011

Can I Buy a Clue, Vanna?

I readily admit that I'm quite ignorant when it comes to macroeconomics. (I was a math major; we try to avoid actual numbers.)

I do know a bit about household (and micro-sized business) finances, given that I have negotiated eighteen book contracts, prepared my own federal and state taxes for several decades, negotiated the sale of our previous condo and purchase of our current house, managed to stay solvent, managed to avoid overdrafts, and managed to stay out of prison. I also worked on the Contracts Committee and the Grievance Committee of Science Fiction and Fantasy Writers of America for several years, delving into other people's contracts and financial disputes.

But as my best buddy Clinton says (I don't mean Bill), a man's got to know his limitations. And as my close pal Donald says (I don't mean Trump), known unknowns are much less dangerous than unknown unknowns. So I cheerfully own that I'm clueless when it comes to the economy of an entire country (or lone superpower, as in the present case -- so far). I'm hoping one of youse readers can comment and explain to me why, in the event that the Republican walk-a-way from the debt-ceiling negotiations becomes permanent, my cockamamie prescription for what to do next is wrongheaded and unworkable.

Here's the setup:

House Majority Leader Eric Cantor pulled out of talks with Vice President Joe Biden on a deficit reduction-debt ceiling deal, saying they had reached an impasse over Democratic demands for tax increases to be paired with spending cuts wanted by the GOP.

The Virginia Republican said in a statement that the Republican-dominated House simply won't support tax increases, and that he wouldn't participate in the budget meeting scheduled for Thursday. Cantor said that it's time for President Barack Obama to weigh in directly on the budget because Democrats insist on negotiating some tax increases.

Sen. Jon Kyl of Arizona, who is representing Senate Republicans in the talks, also dropped out. White House press secretary Jay Carney declared the talks "in abeyance" but said they had been successful in identifying areas of common ground.

Here are the allegedly dire consequences upon epic fail of the talks:

There are only 5 1/2 weeks remaining until an Aug. 2 deadline for enacting an increase in the nation's debt limit to prevent a U.S. default. Economists warn that could damage the nation's credit rating and force the government to pay higher interest rates to continue to borrow the $125 billion a month it needs to finance its operations.

Reuters apes the Associated Press:

Negotiators had hoped to reach a budget deal by next week that would give lawmakers political cover to raise the $14.3 trillion debt ceiling before the Treasury Department runs out of money to pay the country's bills.

Default could occur if Congress does not act by August 2, pushing the United States back into recession and sending markets plunging around the globe.

Now please bear with me, as my main man Pete (I don't mean Sneaky) would say, because I must be making an elementary and risible oops. Anyone with actual training in economics, feel free to leap in with both feet in the fire! But I have long been under the impression that a "default" occurs only when a person, corporation, group, or other entity fails to meet a payment by the mandated deadline.

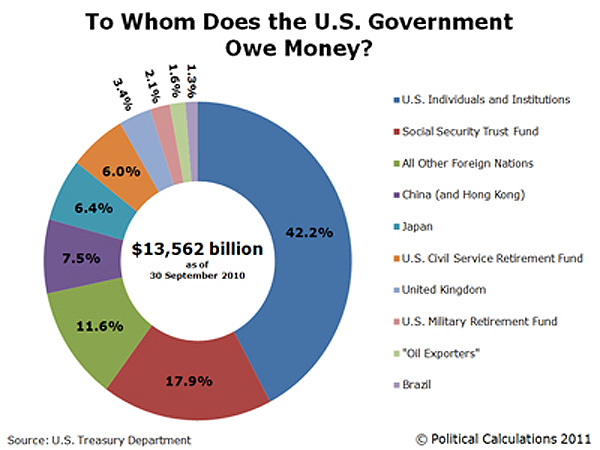

And as I understand (or wildly misunderstand), in the case of a government, "default" only occurs if it fails to pay the interest on its national debt. For the United States, that interest would be the interest on Treasury bills and other debt instruments held by individuals -- mostly American citizens -- or by other countries. Here, look at this chart from Business Insider:

U.S. National Debt Pie Chart

(It's not really germane to the point, but I think it's interesting.)

I've always thought that so long as the interest on T-bills and similar instruments is paid on maturity to Americans and others who own them, we're not in defaut.

My touchstone here is in my personal finances and in the book contracts: Darn near every month, various creditors -- the mortgage company, the gas company, water and power, credit-card companies, car insurance, medical and dental professionals and facilities, the gym, and so forth, send us letters enclosing bills. Each bill lists an amount due and a "pay by" date.

A couple of times a month, I gather all the current bills together and write the creditors a bunch of checks. This money is deducted from our income that month. From the remainder, we pay for food, clothing, gasoline, vodka, and other necessities. Then when all that is allotted, we spend on entertainment, books, CDs, and suchlike frivolities. Finally, whatever still remains we can invest or hold in a savings account or give away to lovable tramps who come to our back door.

You may note, by the order in which I wrote the above, that we always pay the bills first, before spending on anything else. If a particular month has more bills than usual, we spend less on current purchases (duh). If a particular month is lighter in the bill department, we have more disposable income, allowing us to buy more stuff or invest more in stocks or mutuals or gold. But we pay the bills first.

And so long as we pay each creditor by its due date, we're not in default on our debt, and they can't take us to court or jack up our interest rate or otherwise take vengeance against us.

This all seems straightforward to me; but I reckon it must be completely different with a government. Because otherwise there would be a very simple way, a scheme, a strategy to ensure that our government never finds itself in default, thus never suffering the dire consequences that Reuters and AP threaten is about to engulf us, now that House Majority Leader Eric Cantor (R-VA, 100%) and Sen. Jon Kyl (R-AZ, 96%) have "walked away" from the negotiations to raise the limit on the national credit card.

Here is my cunning plan: In the event that the negotiations "collapse," and the debt ceiling isn't raised -- can't Congress simply prioritize paying interest on the national debt?

That is, when it's crafting a budget, can't Congress budget the funds to make any required payments for maturing U.S. national-debt investment instruments, such as T-bills, first, before any other budget item? Once those payments are accounted for, Congress can budget money for other purposes, such as funding departments (Defense, State, etc) and paying federal salaries, funding so-called "entitlement programs," and finally discretionary spending. Why not prioritize interest on the debt over eveything else, just as they prioritize "entitlement" spending over discretionary spending? (The analogy to the household finances is that we pay our bills first, then we pay for necessities, and finally we spend on unnecessaries.)

All right, maybe we wouldn't be able to fund all the discretionary projects we wish we could. But hey, them's the breaks. As Mason said to Dixon, "you gotta draw the line somewhere!" (I don't mean Perry and Cromwell.) But at least the national debt would be serviced, if that's the word I want. (It sounds oddly salacious.)

I realize it can't possibly be that easy, or else Congress would routinely enact a budget like that. Heck, the Democratic Senate hasn't enacted any budget at all since Barack H. Obama became president, so there must be some arcane reason why "pay the interest on the debt first" budgeting isn't possible or feasible for the wealthiest nation in all of human history.

But could somebody please enlighten me as to why not? I hate feeling so completely gormless.

Hatched by Dafydd on this day, June 23, 2011, at the time of 2:37 PM | Comments (9)

March 31, 2011

The Pension Suspension Is Killing Us!

Budget negotiations between California Democrat-retread Gov. Jerry Brown and the legislative Republicans have collapsed. (Surprise, surprise on the Jungle River Boat ride tonight.)

Brown recognizes (or claims to recognize) that the biggest problem in the Leaden State (formerly the Golden State) is too darned much spending; yet for political reasons -- mainly because his own Democratic Party would never accept such a solution -- he doesn't want to close the "$26 billion abyss" in the budget on spending cuts alone. So in addition to proposing some cuts ($11.2 billion, or 43% of the deficit), Brown also seeks to extend a series of "temporary taxes" due to expire this year.

And therein lies the dilemma: Under California's constitution, raising taxes requires a 2/3rds vote in both chambers. But despite Democratic gains in the 2010 elections, the current party mix is as follows:

Lead-in paragraph:

| Chamber | Democrats | Republicans | Votes needed for Democrats to raise taxes |

|---|---|---|---|

| State Senate | 25 (62.5%) | 15 (38.5%) | 2 more votes |

| State Assembly | 52 (65.8%) | 27 (38.5%) | 1 more vote (or 2, if vacancy filled) |

In other words, Democrats alone do not have enough votes to extend those taxes; and so far, the Republicans have held firm, casting not a single vote for the extensions. Besides, again for political cover, Gov. Brown wants the state's voters to approve the tax extension (that is, the tax increase from what current law mandates starting in July). Thus, what the Democrats actually want to pass is a bill that would place on the June 7th, 2011 state ballot an initiative to extend the temporary, two-year tax increases imposed in 2009 for an additional five years. That ballot currently has only local issues; but the legislature can put statewide legislative initiatives onto the ballot if they act by tomorrow, Friday, April 1st, I believe.

(Does anybody doubt that in 2016, Jerry Brown, if he's still governor, or any other Democrat will demand that we "extend" the tax increases for an additional five or ten or twenty years? "With such a whopping huge deficit in 2016," he or she will wail, "we mustn't even think about tax cuts for California fat cats!")

However, at the moment, the Cal-GOP legislators won't give Brown his initiative, either. Nor is it even likely to pass, even if Democrats find a way to shoehorn it onto the June ballot:

The bigger problem is whether Democrats could drum up enough votes among a cash-strapped electorate to pass a tax increase, especially without the backing of any Republican lawmakers.

A Public Policy Institute of California poll released March 23 showed voter support for the proposal waning. While 66 percent of likely voters agreed with the plan in January, only 51 percent still thought it was a good idea by March.

The survey also showed likely voters divided on how to balance the budget, with 41 percent saying they preferred a mixture of cuts and tax increases, and 40 percent favoring the so-called “all-cuts” solution.

“They seem to be convinced it will not pass,” said Tony Quinn, co-editor of the California Target Book in Sacramento. “They’ve probably got internal polling data saying that if they don’t have Republican votes, voters won’t pass it.”

That's a fifteen-point drop in support for the tax extensions in just two months. Most Californios understand that there are three proximate causes for the reality-warping state deficit... and "undertaxation" is not among them:

- The refusal by Democrats to rein in spending on so-called "entitlements," most especially including unfunded public-employee pension plans.

- A stifling regulatory regime, still expanding, that is tying down California businesses like the Lilliputians tying down Lemuel Gulliver with a million regulatory threads... to the point where, as Robert Anton Wilson put it, "Everything not compulsory is forbidden; everything not forbidden is compulsory." And in fact, some forbidden things are nevertheless compulsory, as regulatory worlds collide.

- One of the most business-hating tort environments in the United States suing more and more local companies out of California and into Oregon, Nevada, and other nearby states.

By an amazing coincidence, the three most potent, greedy, and narcissistic special interests within the California Democratic Party are public-employee labor unions, who demand that all pensions and benefits be sacrosanct, no matter how big a hole they blow in the state budget; ultra-liberal government regulators, appropriators, and other rent-seekers, who think Capitalism is out of control and needs to be under the thumb of the State; and plaintiff civil trial-lawyers, who loot the state to the tune of billions of dollars by filing bogus class-action lawsuits and ridiculous personal injury, medical malpractice, and consumer product safety claims (the only lawsuits they seem to have no interest filing are claims of legal malpractice).

And by a second amazing coincidence, those issues are precisely the Rubicon that the Democrats in the state legislature will not cross: public-employee pensions and benefits, regulation and welfare entitlements, and tort reform. Hence the "unexpected" collapse of budget negotiations.

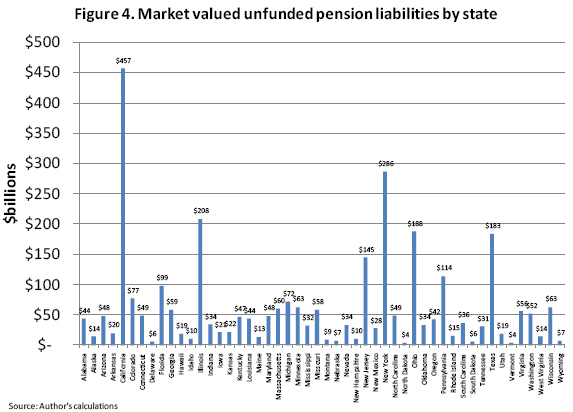

Long term, the biggest problem is probably pensions; in February of last year, the American Enterprise Institute published a detailed calculation of just how much unfunded liability public pensions have dumped on the states, and specifically on California in the present case:

As the largest state, California not surprisingly has the largest absolute public pension funding shortfall at $454 billion, followed by New York with $284 billion and Illinois with $208 billion. Figure 4 shows the market value of unfunded pension liabilities by state.

In case you're interested, here's "figure 4":

Republicans have specifically targeted out-of-control public pension plans, and that is one of the shoals upon which negotiations foundered:

The GOP had pushed for pension reform for public employees, a hard cap on state spending, and a loosening of the state’s regulatory climate. Democrats said the Republican demands were unreasonable, while Republicans blamed the state’s public-employee unions and trial attorneys for sinking the negotiations.

“As a result of these groups’ refusal to challenge the status quo, it has become clear the governor and legislative Democrats are not in a position to work with us to pass the measures necessary to move California forward,” said Republican state Sen. Anthony Cannella in a statement.

So there we are. The California budget is shattered by a budget chasm the size of the Valles Marineris on Mars. The deficit is primarily fueled by public pensions, overregulation, and a trial-lawyer's wet dream of a tort system. But the Democrats utterly refuse to touch any of those three causes, because they would have to defy the most powerful and aggressive special interests within their own party.

The Democrats' solution? Balance the budget on the backs of California taxpayers: When liberals are in charge, Econ. 101 is invariably trumped by Politics 101.

In the end, California voters will have their say; and Gov. Jerry Brown will very likely have to find a way to close the gap without raising taxes that are already unconscionably high. But how long will those same voters who reject tax increases and endless spending nevertheless keep reflexively reelecting the party that is completely and impulsively defined by the mantra "tax, borrow, and spend?"

Hatched by Dafydd on this day, March 31, 2011, at the time of 7:33 PM | Comments (0)

January 20, 2011

A Good Start; Keep Plugging!

The Republican Study Committee, a conservative caucus within the House of Representatives that is chaired by Rep. Jim Jordan (R-OH, 100%), has proposed the Spending Reduction Act of 2011. But before taking a look, let's review the status quo.

Let's recall that the GOP leadership was talking about possibly, maybe, well not quite but close, cutting about $100 billion from the 2011 budget -- that is, cutting approximately 2.6% from total federal outlays as proposed by President Barack H. Obama in 2010. And let's also understand that the total Obama proposed includes hundreds of billions of dollars in fantasy spending cuts that the Left would never actually implement, coupled with hundreds of billions of dollars in "off-line" spending that is separately accounted. Realistically, real spending would likely be closer to $4.5 trillion under the generous hand of the Obamunist (always willing to dig down deep in your pocket and take until it hurts). So on Planet Earth, the Republican leadership is really talking about a robust 2.2% reduction. Wow.

Now back to the RSC's proposal; they begin with a much bolder goal:

Moving aggressively to make good on election promises to slash the federal budget, the House GOP today unveiled an eye-popping plan to eliminate $2.5 trillion in spending over the next 10 years. Gone would be Amtrak subsidies, fat checks to the Legal Services Corporation and National Endowment for the Arts, and some $900 million to run President Obama's healthcare reform program.

What's more, the "Spending Reduction Act of 2011" proposed by members of the conservative Republican Study Committee, chaired by Ohio Rep. Jim Jordan, would reduce current spending for non-defense, non-homeland security and non-veterans programs to 2008 levels, eliminate federal control of Fannie Mae and Freddie Mac, cut the federal workforce by 15 percent through attrition, and cut some $80 billion by blocking implementation of Obamacare.

(I've put the entire list of cuts, from the RSC Overview of their spending-cut proposal, in the extended portion of this post; click the "Slither on.")

Dividing $2.5 trillion by ten years yields an annual reduction (from proposed budgets) of $250 billion, two and a half times what the GOP top dogs first proposed, then walked back. Another way to look at it is that, instead of a yearly 2.2% reduction of the real spending mountain we face, the RSC proposes a yearly reduction of 5.6%.

So as I said, a good start. But there is another benefit if this proposal or anything close were enacted, perhaps after a lengthy negotiation with frightened Democrats; it would demonstrate that we can cut spending.

Actual spending reduction (as opposed to a reduction in the increase) is as rare as a Democrat with callused hands. Ronald Reagan and George W. Bush were able to significantly reduce taxes, but never spending. Bill Clinton, in concert with a newly Republican Congress (both houses), was able to balance the budget, but primarily by the fortuitous explosion of the computer/high-tech industry, which expanded the tax base... which itself had more to do with economic and regulatory policies initiated by Reagan than anything Clinton did. But I cannot recall significant spending cuts in my lifetime.

(Checking the budget history, there was a major spending reduction when World War II ended -- we were no longer supporting seven million men in the field, fighting half the world -- and a small reduction when the Korean War ended. But spending rose continuously throughout the Vietnam War and kept on rising after the war ended, not with a bang but a bug-out.)

Many Americans, having no experience with actually cutting spending from year to year, simply accept as read that it's impossible; but if we can demonstrate it before our very unbelieving eyes, then maybe folks will get all het up about cutting more and more and more. What Man has done, men can aspire to do!

With courage, perseverence, and good argument, we might be able to slash spending further and deeper than this nice jumping-off point from the RSC, down to a level that is actually comprehensible to mortal humans; at the very least, we should be able to slash Obama's ten-year deficit from $10 trillion to, say, only $3-4 trillion. And from there, it's only a short hop to a real balanced budget. And this time, once we have achieved balance through spending cuts, not tax increases, maybe we'll be diligent enough to keep it there.

On the other hand, if this proposal comes to nought; if it's watered down by the Republican nomenklatura in the House; blocked by the Democrats in the Senate; summarily rejected without even a nod towards negotiation by la Casa Blanca; and tossed in the dustbin of history... then it will have the opposite effect: It will confirm the initial thesis, that real spending cuts are literally impossible.

So this is very high-stakes political poker, and we're all-in on this one. Let's hope the RSC isn't just playing a stone bluff.

A complete listing of the spending cuts proposed by the Republican Study Committee

- FY 2011 CR Amendment: Replace the spending levels in the FY 2011 continuing resolution (CR) with non-defense, non-homeland security, non-veterans spending at FY 2008 levels. The legislation will further prohibit any FY 2011 funding from being used to carry out any provision of the Democrat government takeover of health care, or to defend the health care law against any lawsuit challenging any provision of the act. $80 billion savings.

- Discretionary Spending Limit, FY 2012-2021: Eliminate automatic increases for inflation from CBO baseline projections for future discretionary appropriations. Further, impose discretionary spending limits through 2021 at 2006 levels on the non-defense portion of the discretionary budget. $2.29 trillion savings over ten years.

- Federal Workforce Reforms: Eliminate automatic pay increases for civilian federal workers for five years. Additionally, cut the civilian workforce by a total of 15 percent through attrition. Allow the hiring of only one new worker for every two workers who leave federal employment until the reduction target has been met. (Savings included in above discretionary savings figure).

- "Stimulus" Repeal: Eliminate all remaining "stimulus" funding. $45 billion total savings.

- Eliminate federal control of Fannie Mae and Freddie Mac. $30 billion total savings.

- Repeal the Medicaid FMAP increase in the "State Bailout" (Senate amendments to S. 1586). $16.1 billion total savings.

- More than 100 specific program eliminations and spending reductions listed below: $330 billion savings over ten years (included in above discretionary savings figure).

Additional Program Eliminations/Spending Reforms

- Corporation for Public Broadcasting Subsidy. $445 million annual savings.

- Save America's Treasures Program. $25 million annual savings.

- International Fund for Ireland. $17 million annual savings.

- Legal Services Corporation. $420 million annual savings.

- National Endowment for the Arts. $167.5 million annual savings.

- National Endowment for the Humanities. $167.5 million annual savings.

- Hope VI Program. $250 million annual savings.

- Amtrak Subsidies. $1.565 billion annual savings.

- Eliminate duplicative education programs. H.R. 2274 (in last Congress), authored by Rep. McKeon, eliminates 68 at a savings of $1.3 billion annually.

- U.S. Trade Development Agency. $55 million annual savings.

- Woodrow Wilson Center Subsidy. $20 million annual savings.

- Cut in half funding for congressional printing and binding. $47 million annual savings.

- John C. Stennis Center Subsidy. $430,000 annual savings.

- Community Development Fund. $4.5 billion annual savings.

- Heritage Area Grants and Statutory Aid. $24 million annual savings.

- Cut Federal Travel Budget in Half. $7.5 billion annual savings.

- Trim Federal Vehicle Budget by 20%. $600 million annual savings.

- Essential Air Service. $150 million annual savings.

- Technology Innovation Program. $70 million annual savings.

- Manufacturing Extension Partnership (MEP) Program. $125 million annual savings.

- Department of Energy Grants to States for Weatherization. $530 million annual savings.

- Beach Replenishment. $95 million annual savings.

- New Starts Transit. $2 billion annual savings.

- Exchange Programs for Alaska, Natives Native Hawaiians, and Their Historical Trading Partners in Massachusetts. $9 million annual savings.

- Intercity and High Speed Rail Grants. $2.5 billion annual savings.

- Title X Family Planning. $318 million annual savings.

- Appalachian Regional Commission. $76 million annual savings.

- Economic Development Administration. $293 million annual savings.

- Programs under the National and Community Services Act. $1.15 billion annual savings.

- Applied Research at Department of Energy. $1.27 billion annual savings.

- FreedomCAR and Fuel Partnership. $200 million annual savings.

- Energy Star Program. $52 million annual savings.

- Economic Assistance to Egypt. $250 million annually.

- U.S. Agency for International Development. $1.39 billion annual savings.

- General Assistance to District of Columbia. $210 million annual savings.

- Subsidy for Washington Metropolitan Area Transit Authority. $150 million annual savings.

- Presidential Campaign Fund. $775 million savings over ten years.

- No funding for federal office space acquisition. $864 million annual savings.

- End prohibitions on competitive sourcing of government services.

- Repeal the Davis-Bacon Act. More than $1 billion annually.

- IRS Direct Deposit: Require the IRS to deposit fees for some services it offers (such as processing payment plans for taxpayers) to the Treasury, instead of allowing it to remain as part of its budget. $1.8 billion savings over ten years.

- Require collection of unpaid taxes by federal employees. $1 billion total savings.

- Prohibit taxpayer funded union activities by federal employees. $1.2 billion savings over ten years.

- Sell excess federal properties the government does not make use of. $15 billion total savings.

- Eliminate death gratuity for Members of Congress.

- Eliminate Mohair Subsidies. $1 million annual savings.

- Eliminate taxpayer subsidies to the United Nations Intergovernmental Panel on Climate Change. $12.5 million annual savings.

- Eliminate Market Access Program. $200 million annual savings.

- USDA Sugar Program. $14 million annual savings.

- Eliminate the National Organic Certification Cost-Share Program. $56.2 million annual savings.

- Eliminate fund for Obamacare administrative costs. $900 million savings.

- Ready to Learn TV Program. $27 million savings.

- HUD Ph.D. Program.

- Deficit Reduction Check-Off Act.

Subsidy to Organisation for Economic Co-operation and Development (OECD). $93 million annual savings.

TOTAL SAVINGS: $2.5 Trillion over Ten Years

Hatched by Dafydd on this day, January 20, 2011, at the time of 6:04 PM | Comments (0) | TrackBack

October 19, 2010

"Not Responsible for Advice Not Taken"

Credit where it's due: That phrase is one of Larry Niven's favorite sayings. (I don't know whether he made it up or heard it somewhere.)

The advice in this case comes from many economists, including Thomas Sowell and Walter Williams, and I'm sure Milton Friedman and Henry Hazlitt had something to say about it: The real-world effect of minimum-wage laws is not to raise incomes -- but to depress employment, thus killing the incomes of the very people the Left purports to protect.

The classical theory is pretty clear: What you subsize, you get more of; what you tax, you get less of. Suppose you're an employer, and you need to hire some guys... for example, teenagers to work in your pizza joint. Taking into account your profit margin, your customer base, and your competition, you determine each employee is worth, say, $5 per hour. But then the Feds -- or more often, your state -- decides that in order to preserve the "dignity of labor," it must impose a minimum wage of, say, $8 per hour (California's rate).

The difference of $3 per hour constitutes the economic equivalent of a 60% tax on labor: By making each worker 60% more expensive than he otherwise would be, the minimum-wage law reduces employment: Where you planned to hire four employees for an extra $20 per hour total, now that same $20 will only buy you two and a half employees... which translates either to two employees instead of four, each stretched pretty thin; or else three employees, and your profit margin (never very high) goes out the window. In either case, you get a significant increase in unemployment, especially among teenaged workers, low-income workers, and low-skilled workers... the very people the law ostensibly is designed to protect and support.

(The labor costs even for higher-paid workers also increases, as many union contracts mandate salaries of all unionized employees at some fixed multiple of the minimum wage.)

That's the classical theory; but a handful of studies by more "progressive" economists in the Clinton 1990s purported to show that decades of classical theory were wrong... and in fact, minimum wage laws and increasing the minimum wage were either neutral on employment -- or actually increased employment! Wow, we could have our tax and eat it, too.

Authors studied several minimum-wage increases in this or that state, compared them to nearby states, and concluded that no evidence showed increased unemployment in the states whose minimum wage had risen, relative to those states whose minimum wage had remained the same.

But during this last decade of the oughts, grave doubt has been cast on these recent studies by even newer research. The basic criticism, I believe, is sound: The question about minimum-wage laws is not whether they exist, but whether a particular minimum is "effective" at raising wages significantly: If not, then employers can absorb the minor cost increase and make it up in other ways; but when it is, when the increase is too big to skirt, then classical theory kicks in and employment drops.

And of course, if a minimum wage increase is too small to significantly impact wages -- then what's the point, exactly?

Suppose you decide to hire those four employees at $5 per hour; but then the government imposes a minimum wage -- of $5.15 per hour, a 3% increase over what you expected to pay. That means instead of a direct labor increase of $20 per hour for your four new employees, you must pay $20.60.

But with a difference of only sixty cents per hour total, you can probably still hire all four employees; you'll just raise prices by 3% or so to make up for it, or you'll slightly decrease the hours your employees work, or some other substitution for not hiring.

But if the minimum wage is raised significantly more, then you can no longer pass the cost along to customers or just make everybody work less; there's not enough slack to stretch that far. Your only option is to cut back employment, which means cutting back services, which means a gigantic slowdown in the economy.

So why did research back in the 90s find what they found? Because, as it happens, states don't normally make drastic, overnight increases in the minimum wage; so the studies were looking at reasonably small increases over the prevailing wage -- which, not surprisingly, did not always cause statistically significant increases in unemployment. Still, it would be nice to have a case study proving what seems obvious in the classical theory: Make labor expensive enough, and business will significantly reduce employment.

What we really need in order to test the classical theory is to have a much more drastic wage increase mandated by government, then see whether that does or does not send the unemployment rate skyrocketing; but such an experiment could be so grotesquely destructive of the economy that nobody but a complete idiot or a madman would champion such a scheme.

Cue the Democratic Congress elected in 2006.

One of the first orders of business of the 110th United States Congress, which took office on January 3rd, 2007, was to raise the federal minimum wage from $5.15 to $7.25 per hour, a 40.8% increase, in three stages of 70 cents each: up to $5.85 in 2007, to $6.55 the next year, and the full $7.25 in 2009.

Coincidentally, the U.S. unemployment rate rose from 4.6% in January, 2007 to 4.9% one year later (an increase of 6.5%); then up to 7.6% by January, 2009 (an increase of 55%); then to 9.7% this last January (another 28% increase), where it has more or less stayed all year. The total increase in unemployment under the Democratic Congress has been 108.7%.

Obviously, you can't attribute the entire surge in unemployment on the drastic increase in the minimum wage; but circumstantial evidence certainly makes it seem likely that the policy must shoulder at least some of the blame. ("Not responsible for advice not taken.")

But the effect of minimum-wage laws can be seen even more transparently when minimum wages designed for the First-World United States are applied, willy-nilly, to its effectively Third-World territories. One of the other provisions of the Democrats' minimum-wage debacle in 2007 was to force the same rule to apply to American Samoa and the Northern Mariana Islands.

As Walter Williams notes, prior to the 110th Congress, the minimum wage in American Samoa was $3.26 per hour; thus the Democratic scheme to increase wages to a minimum of $7.25 per hour amounted to a 122.4% "raise" for all workers in that territory. Surprise, surprise, even though the law is being phased in at fifty cents per hour per year (slightly slower than in the United States) and hasn't gotten anywhere near the looming peak, the net result has been to devastate the Samoan economy, particularly the tuna canneries:

Chicken of the Sea International moved its operation from Samoa to a highly automated cannery plant in Lyon, Georgia. That resulted in roughly 2,000 jobs lost in Samoa and a gain of 200 jobs in Georgia.

Given Samoa's low cost of living, $3.26 provided Samoan workers a higher standard of living than some of their neighbors on other islands. Now these workers are unemployed. What's worse is that Starkist, Chicken of the Sea's competitor, might leave the island as well. If that happens, increases in the minimum wage will have cost more than 8,000 jobs in Samoa's canneries and related industries; that's nearly half of its labor force.

And now, the Democrat-induced extreme labor surplus in Samoa has become so glaringly obvious, even the Democratic Congress has (reluctantly) noticed and been forced (even more reluctantly) to undo its own "progressive" scheme:

Just three years after a Democrat-led Congress imposed the federal minimum wage on two U.S. territories in the Pacific, lawmakers last month halted the program in its tracks, acknowledging the move had sapped thousands of jobs from American Samoa and the commonwealth of the Northern Mariana Islands.

The two-year delay in the case of American Samoa and one-year reprieve for the Northern Mariana Islands was imposed even as both parties have sparred over the effects of the minimum wage in the U.S. during the troubled economy.

"We said this increase would be harmful in 2007, and the Democrats did it anyway," said Rep. Patrick T. McHenry, North Carolina Republican. "It proves our point that the federal government setting wage rates is destructive to job creation, whether it's in American Samoa or western North Carolina."

So it appears that classical economics theory is still valid; not even so eminent a liberal as the One We Had Supposedly Been Awaiting All This Time can repeal the basic relationship between marginal cost and supply and demand, of labor or any other commodity: By making labor more expensive, you reduce its demand and therefore increase unemployment. And the more expensive you make labor, the higher you drive unemployment (take a long look at Europe).

I believe the experience of the last few years of Democratic control of Congress and (after the 2008 election catastrophe) the White House should cause even ultra-liberal economists, such as Paul Krugman, to rethink their tendentious rejection of any linkage between (a) increasing the cost of doing business, and (b) decreasing the amount of business being done... and in particular their risible contention that increasing the cost of labor actually reduces unemployment.

But I would put the odds that even the hardest reality can penetrate the liberal-progressive-socialist body armor of faith-based ideology at somewhere south of zero. Perhaps instead of teaching college students the joys of Keynesian economics -- or worse, Alinskyism -- universities should make every student read and pass a comprehension test on the classic sociology book When Prophecy Fails, chronicling how true believers in a UFO cult react when their date for the end of the world comes and goes, but Earth abides.

(Study hint: A few cultists peeled off, but most not only remained they picked a newer, later date for world destruction -- and redoubled their efforts to proselytize for new members! Sound familiar?)

Hatched by Dafydd on this day, October 19, 2010, at the time of 3:08 PM | Comments (1) | TrackBack

September 24, 2010

The New Girls Network

The Tea Party has always been predominantly a women’s movement, or else they would have called it the “beer party.” Because of the high profile of Tea Party types like Glenn Beck, it is easy to forget that those frequently taking the point in reforming the Republican Party -- and the nation itself -- are outsiders like Sarah Palin and her “constipated grizzlies,” or whatever she calls them.

The latest of eight almost unbroken series of Tea Party victories in Republican primaries -- against candidates endorsed by the National Republican Senate Committee -- was racked up last week by Christine O'Donnell of Delaware, who is reminiscent of Palin, but without her laserlike intellectual firepower.

But you don’t need a big brain -- although perhaps a big mouth helps -- if your message is simple: cut spending, get big government out of our lives, and cut taxes.